Many corporate finance models that model how a single company’s balance sheet changes over time use DSO (days sales outstanding) as an input assumption. So as an input assumption it drives pro forma A/R (accounts receivable) levels and period-over-period cash flows directly. And to fine tune these outputs, you manipulate the DSO number directly. In this article we will explore why using DSO as an input is often not desirable, and we should seek to evaluate DSO as an output using another method to model A/R.

Example: In our method comparison example model (available in Downloads: DSOs_as_Output_v2.xlsx), we provide an example of how much A/R can vary depending on how you change the projection method, with the same revenue inputs.

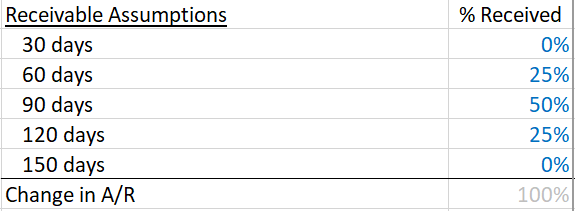

In Method 1, we use DSO as the input. In Method 2, we use a receipt-based method as the input (Figure A), bucketing the receivables into categories – in real life these categories would correspond to %s of customers with those payment terms (and a history of paying on-time!).

For Method 1, we use 90 days DSO as an input. For Method 2, we use an average receipt of 90 days – but with 25% received in 60 days, 50% received in 90 days and, 25% received in 120 days as inputs.

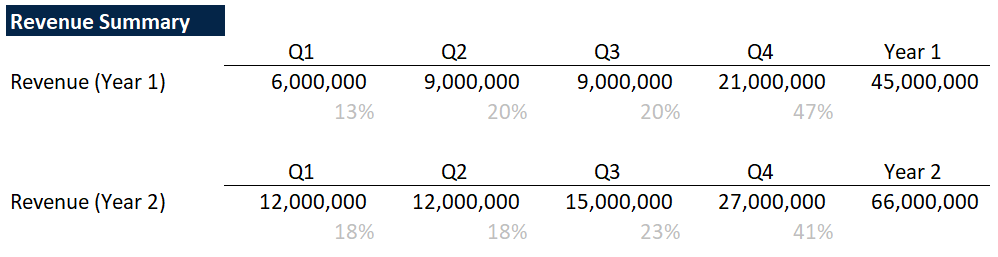

The Revenue across both methods is the same – in Year 1, 45M, in Year 2, 66M. There is monthly variation with heavy Q4 seasonality for illustrative purposes (Figure B).

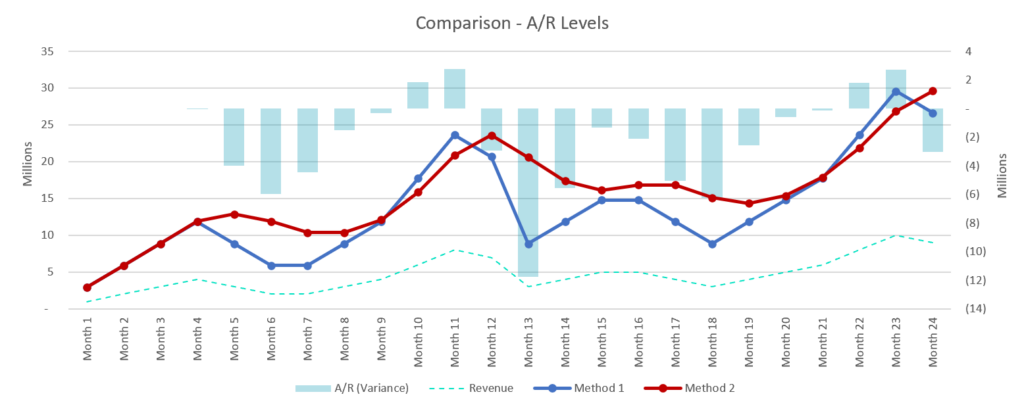

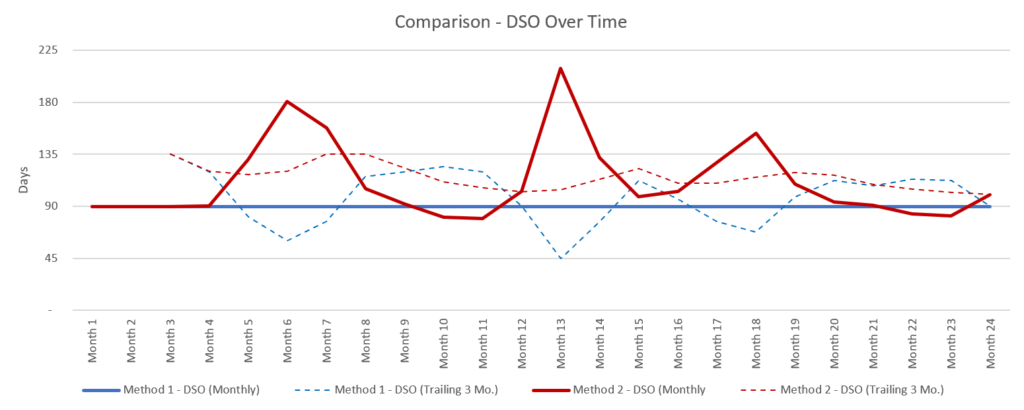

These are not mathematically equivalent, but that’s sort of the point. The graph (Figure C) shows the differences in A/R levels over time. The embedded bar chart shows that in one period (Month 13) there is a 11.75M difference in A/R between the two methods! Given the revenue levels, that’s a massive variance. The difference in DSO over time is just as stark, especially in certain periods (Figure D).

Contextual factors: Choosing which method to use depends on many factors specific to the business you’re evaluating – stage in the life cycle of the business, rate of revenue growth, seasonality, customer concentration, contractual invoice terms, etc. In our opinion, periods of heavy growth or large seasonal swings in revenue require a bit more care in modeling and we would lean towards using a more granular receipts-based method over a blunt DSO-as-an-input method. As you can see by running different scenarios in the method comparison example model, large month-over-month changes in revenue can result in large discrepancies between each A/R modeling method.

Implications: It’s also worthwhile to consider what this model is being used for in selecting and fine tuning a method and its related assumptions. For example, if the business is planning to raise money via a receivables-based line of credit from a bank or other institution, any such line of credit may come with loan covenants attached to A/R levels. So making sure your pro forma modeling of A/R is as realistic as possible can be critical to ensure proper loan comparison, covenant calculations, and continued funding.

If you have a more complicated use case, you can also set things up so that you can transition in between different methods seamlessly over time. This is useful for startups or certain types of pro forma models where there is only partial information or less detail is needed for certain time periods within the same model. So enjoy fine tuning using this example, and leave us a comment on something you do differently.